Since the beginning of this year, the central government has continued to respond to the international financial crisis and has accelerated the process of economic development by changing a series of policies and measures. The industrial economy has generally continued its upward trend in the second half of last year and has continued to develop in the expected direction of macroeconomic control. Industrial production maintained rapid growth. The business operations of the enterprises have been significantly improved, foreign trade exports have been accelerated, energy conservation and emission reduction, elimination of backward production capacity have steadily progressed, and structural adjustments and changes in development methods have made positive progress.

I. Basic situation of industrial economic operation since this year

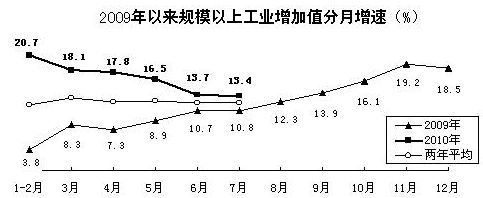

(1) The high growth rate of production moderately decreased, energy-saving and emission-reduction, elimination of outdated and other active regulation effects were obvious, and the growth rate of high energy-consuming industries fell sharply. From January to July, the industrial added value of industrial enterprises above designated size increased by 17% year-on-year, and the growth rate increased 9.5 percentage points year-on-year, with 19.6% in the first quarter, 15.9% in the second quarter, and the rate of growth in the two months of June and July dropped to 13.7% respectively. And 13.4%. If we consider the effect of the same period last year, with the same period in 2008 as the base period, the average growth rate in the past two years from January to July was 12.1%, of which the growth rate in the first quarter was 12.1%, the growth rate in the second quarter was 12.4%, and both in June and July. The monthly growth rates were 12.2% and 12.1% respectively, and the stability of economic operation was further consolidated. In terms of light and heavy industries, from January to July, the value added of light and heavy industries increased by 13.6% and 18.4% year-on-year, respectively, accelerating 5.5 and 11.2 percentage points year-on-year, respectively, of which the growth rate was 13.5% and 13.3% respectively in July. In heavy industry, 0.2 percentage points changed the growth trend of heavy industry since June of last year for 13 months in a row faster than that of light industry. The pull of light and heavy industries on economic growth has further tended to be coordinated.

After the State Council's energy-saving and emission-reduction video-telephone conference, all localities and departments have stepped up efforts to reduce energy consumption, eliminate backward production capacity, and curb excessive growth in high-energy-consuming industries. From January to July, the growth rate of the six high-energy-consuming industries decreased from 19.6% in the first quarter to 16.2%, of which 10.5% in July, 1.3% slower than the previous month, and the rate of decline was faster than that of all industries above designated size. Percentage. As the growth rate of high-energy-consuming industries has accelerated, the momentum of excessive growth in industrial energy consumption has begun to slow. The energy consumption per unit of value has changed from a year-on-year increase of 0.38% to a year-on-year decrease of 1.25%. According to statistics from China Federation of Electric Power Enterprises, from January to July, the industrial electricity consumption in the country increased by 22.6% year-on-year, an increase of 5 percentage points from the first quarter; of which, the national industrial electricity consumption in July increased by 15.3% year-on-year, 0.4% lower than the previous month. Percentage.

(II) The business conditions of the enterprises continued to improve, taxpayers and the ability to absorb employment were further strengthened, and the operating status of SMEs was improved. From January to July, the accumulated profits of industrial enterprises above designated size (82.1% of total scale industries from January to July in the 24 provinces and counties counted by the National Bureau of Statistics) increased by 61.1% year-on-year, and the sales profit rate was 5.15 from the same period of last year. % rose to 6.16%, total taxes paid increased by 29.9% compared to the same period of last year, and the average number of employees rose by 6.7% year-on-year.

The production of SMEs has accelerated, and the business conditions have further improved. From January to July, the added value of small and medium-sized enterprises above designated size increased by 18.2% year-on-year, 1.2% faster than the average level of all industries above designated size. From January to May, small and medium-sized enterprises above designated size achieved a profit of 966.6 billion yuan, and paid tax totaled 57.2 billion yuan, up by 72.2% and 28.7% year-on-year respectively, accounting for 63% and 51.4% of the total industrial size of all industries above the designated size; 66.73 million people, an increase of 4.39 million over the same period last year, an increase of 7%.

(3) Domestic demand has grown steadily, and foreign trade exports have gradually recovered. From January to July, the output value of industrial enterprises above the designated size increased by 32.4% year-on-year, of which domestic sales increased by 33.1%, accounting for 86.8% of the total sales value, which was 0.5% higher than the same period of 2009 and higher than the same period of 2008 and 2007 respectively. 3.4 and 5.2 percentage points. With the fall in the growth rate of fixed asset investment, the growth rate of production of investment products has slowed down significantly, and the pulling effect of consumption on industrial growth has increased. From January to July, the contribution of the domestic sales value of consumer goods industry to the growth of domestic industrial output value of all above-scale industries rose to 23.5%, 0.7 and 1.4 percentage points higher than the first half and first quarter, respectively.

Exports accelerated at a lower base last year. From January to July, the export value of industrial exports above designated size increased by 28.2% year-on-year, 8.2% over the same period of 2008, of which from January to February increased by 3.2% over the same period of 2008, and 3, 4, 5, 6, and 7 months. Compared with the same period in 2008, they increased by 8.1%, 9.3%, 11.9%, 12.3% and 9.1% respectively. According to customs statistics, from January to July, China's foreign trade exports totaled 855.5 billion U.S. dollars, an increase of 35.6% year-on-year and an increase of 5.8% over the same period of 2008. If factors such as the depreciation of the U.S. dollar were taken into consideration, the level of the same period before the international financial crisis has not fully recovered.

(4) The industrial investment structure has been improved, and technological transformation has strengthened the industrial pull. From January to July, the country’s industrial fixed asset investment increased by 22.1% year-on-year, with the growth rate down 5.1% year-on-year; of which, manufacturing investment increased by 25.1%, which was 0.7 percentage point lower than the first quarter, and the investment growth of the six high energy-consuming industries from the same period of last year 23.8% fell to 15.3%. The role of technological transformation in promoting the development of industrially-integrated development has increased. In 2009, the central government issued 4441 special interest subsidy projects for technical transformation projects. All projects have been started. The total planned investment is 632.6 billion yuan. By the end of May, the accumulatively invested capital was 421.9 billion yuan, and the investment reached 344.3 billion yuan; the project has been completed and put into production 662 projects. Invested 63.8 billion yuan. Local governments have always attached importance to technological transformation and industrial restructuring has clearly benefited from the investment in technological reforms. According to incomplete statistics, the funds used by local provincial-level local governments for technical reform last year amounted to about 20 billion yuan.

(5) Positive results have been achieved in the adjustment and revitalization of key industries, and it is evident that the crisis will play a role in maintaining growth. At the beginning of 2009, the State successively formulated plans for the adjustment and revitalization of ten key industries such as automobiles, steel, textiles, equipment manufacturing, shipbuilding, electronic information, light industry, petrochemicals, non-ferrous metals, and logistics. Over one year of planning and implementation has achieved remarkable results. In the first seven months of this year, the value added of the nine industrial sectors involved in the adjustment and revitalization of key industries was 17.2% year-on-year, and that of the first five months was 1.13 trillion yuan, an increase of 84.8%. The industrial structure adjustment has made new progress. In particular, the State Council's opinions on further strengthening the elimination of backward production capacity, accelerating the promotion of corporate mergers and reorganizations, and advancing the implementation of a series of industrial policies such as accelerating the structural adjustment of the steel industry and promoting the healthy development of the industry have accelerated the merger and reorganization of enterprises and eliminated backward steps. The merger and reorganization of the iron and steel industry proceeded in an orderly manner. This year, Ben Steel merged with Beitai Iron and Steel, Shougang merged Tonghua Steel, Anshan Iron and Steel and Panzhihua Iron & Steel achieved a joint restructuring, and Tianjin Iron & Steel Co., Ltd. was jointly established by four steel companies in Tianjin. After the automobile production and sales volume exceeded 10 million units in 2009, it also reached 10.21 million units and 10.26 million units from January to July this year, an increase of 43.6% and 42.7% year-on-year. In the first 7 months, the national shipbuilding completed capacity reached 35.20 million dwt, an increase of 87.4% over the same period of last year. Due to the rapid recovery of new orders, the amount of hand-held orders in the industry reached a level with the end of 2009.

(6) The coordinated development of the regional economy, and the high-tech industry has a good momentum of development. From January to July, the industrial added value of above-scale industries in the East, Central and West regions increased by 16.1%, 19.9%, and 16.9% year-on-year, respectively. The proportion of the central and western regions that accounted for the added value of industries above designated size increased from 37.7% in the same period of 2008 to 38.9. %. The added value of high-tech industries increased by 17.7% year-on-year, 0.7% higher than that of all industries above designated size, of which biopharmaceuticals and biochemicals increased by 18.9%, integrated circuits increased by 34.7%, electronic computers and office equipment increased by 17.9%, medical equipment and instrumentation. Increased by 18%. From January to July, software business revenue increased by 29%, an acceleration of 6.8 percentage points year-on-year.

II. Main difficulties and problems facing the current operation of the industrial economy

At present, the operation of the industrial economy is in a critical period of transition from a rebound to a good and sustained and stable growth. There are many favorable conditions for continuing to maintain a steady and rapid development of the industrial economy. However, there are also many difficulties and problems faced. In particular, unstable and uncertain factors in the economic operation have obviously increased. Short-term problems and long-term conflicts are intertwined. Domestic factors and international Factors interact with each other, and the internal and external environments of the economy are complex and changeable. It is necessary to plan ahead and respond positively.

(I) The foundation of global economic recovery remains fragile and export pressures increase

At present, the unemployment rate in Europe and the United States is still in the high range of 9%-10%. The level of deficits in major countries is extremely high. It is estimated that the U.S. government deficit will account for 10% of GDP this year, the average level of the 16 countries in the euro zone will reach 7%, and Japan will have to reach 19%. High debt-repayment rates will cause governments to tighten their fiscal expenditures. The total demand is greatly compressed. The continuation of the European sovereign debt crisis may exacerbate the depreciation of the euro against the US dollar and the renminbi. Since April of this year, the appreciation of the renminbi against the euro has approached 15%, which has brought greater pressure on domestic exporters. The European debt crisis in the coming months will affect China’s foreign trade. The negative effects of exports may gradually appear. Trade remedy measures against China have significantly increased. In the first quarter of this year, the world launched 19 new anti-dumping investigations and 15 newly launched trade protection policies, including 9 and 10 for China's exports, respectively, accounting for 47% of the total. 67%, the trend of international trade protectionism has intensified. In the first half of the year, there were 38 international trade remedy measures against China, including 7 cases in the EU, involving a total of US$4.6 billion.

(2) The slowdown in investment growth and the long-term mechanism for the investment in technological transformation of enterprises need to be established.

From January to July, investment in urban fixed assets rose by 24.9%, down 8 percentage points year-on-year and 0.6 percentage points lower than the first half. According to the statistics provided by the National Bureau of Statistics, the investment for reconstruction in the first half of this year has accumulatively completed 1.23 trillion yuan, an increase of 21.1% year-on-year, and 7.7 percentage points lower than the new investment. The reconstruction investment accounts for only 12.5% ​​of the entire society's fixed asset investment. At present, the pattern of technological transformation work that the central government attaches great importance to, local support, and enterprises welcome and social concerns has taken shape. It is necessary to improve and innovate the method of discounting technological innovations, guide enterprises and local governments to increase investment in technological reforms, revitalize stock assets, and accelerate the realization of connotative development. Accelerate the establishment of a long-term mechanism, further improve the management of technological transformation, streamline management relationships, and give full play to the important role of technological reforms in improving the quality of business operations and the transformation of economic development.

(III) Difficulties in eliminating obsolete production capacity and suppressing redundant construction, and facing greater difficulties in structural adjustment

The repeated construction of some traditional industries such as steel, cement, coal chemical industry, and flat glass has caused serious vicious competition. The issue of excess production capacity is outstanding, and backward production capacity still occupies a considerable proportion. Wind power equipment, polysilicon and other emerging industries also have signs of blind construction. At present, the domestic polysilicon project has a designed capacity of more than 40,000 tons, and the project under construction has a designed capacity of more than 60,000 tons, totaling about 100,000 tons. With the improvement of domestic and foreign market demand, and at the same time as structural adjustments affect all aspects of interests, in particular the elimination of backwardness and mergers and reorganizations are highly policy-oriented, involve a wide range, and organization and coordination are very difficult, requiring institutional mechanisms to reform and innovate. Big.

(4) The task of saving energy and reducing consumption is heavy, time is tight, and pressure is high

Since the third quarter of 2009, with the gradual recovery of China's economy, the high energy-consuming and high-emission industries have grown rapidly, making the unit value-added energy consumption rise instead of fall. In the first seven months of this year, the value added of heavy industry increased by 18.4% year-on-year, 4.8 percentage points faster than that of light industry, of which the increase value of six high energy-consuming industries increased by 16.2% year-on-year; the industrial electricity consumption increased by 22.6% year-on-year, of which light and heavy industries Electricity increased by 13.5% and 24.6% respectively, and the proportion of electricity used by heavy industry reached 83.8%, which was 1.3% higher than the same period of last year. In the first quarter of this year, the energy consumption of units with a size above designated size increased by 0.38% year-on-year, while it fell by 1.25% in the first half of the year, but the decrease was modest. The task of saving energy and reducing consumption in the following months was arduous. At present, the State Council has organized six inspection teams to go to 18 key regions for supervision and inspection of energy conservation and emission reduction work to ensure that local governments intensify efforts to ensure the completion of the “Eleventh Five-Year†energy saving and emission reduction tasks.

(5) The business environment is complex and changeable, and the difficulty of production and operation of the company increases

First, energy and raw material prices have risen rapidly, and labor pressure has increased. From January to July, the ex-factory price of industrial products rose by 5.8% year-on-year, while the purchasing prices of raw materials, fuel, and power increased by 10.5% year-on-year, of which the purchase price of fuel and power rose by 21.3%. Since the beginning of this year, wage costs in the coastal areas such as the Yangtze River Delta and the Pearl River Delta have generally risen by 20%-25%. Second, the voice of SMEs to reflect financing difficulties has increased. Although commercial banks have adopted a separate arrangement for small businesses to increase the size of new credits, a separate assessment method has been adopted to steadily and orderly promote the development of small and medium-sized financial institutions such as village and town banks, loan companies, and mutual aid cooperatives. However, it is difficult for SMEs to face difficulties in financing. Within this period, substantial improvements have been achieved. The bank deposit reserve ratio has been raised three times in a row since the beginning of this year. Corporate financing costs have increased, and SME financing has become even more prominent. The third is the increased anticipation of instability in exports. Processing-manufacturing companies, especially labor-intensive ones, which are mainly export-oriented, are affected by fluctuations in exchange rate expectations, and they are afraid to accept large orders or long-term orders. The fourth is the impact of extreme drought and floods. In the spring of this year, major droughts occurred in the southern provinces. Water shortages and electricity shortages led to the suspension of new renovations and expansion projects or delayed production. Since the beginning of summer, natural disasters such as storms, floods and mudslides have occurred in Guangxi, Jiangxi, Gansu, Shaanxi, Jilin, and other places, causing serious losses to the production and operation of industrial enterprises. Fifth, since the beginning of this year, despite the initial effect of the new real estate control policy, the overall price of housing is still running at a high level, and the transaction volume has shrunk dramatically. The impact on the operation of the industrial economy cannot be ignored.

Third, the annual economic operation will show the trend of “high before and after lowâ€

Judging from the current operating situation, due to the impact of last year's "low before and after high" trend, the industrial growth rate in the second half of the year will decline to a certain extent, and is expected to drop to about 10% in the second half of the year, and it can still reach about 13% in the whole year. Mainly based on the following aspects of the judgment: First, from the perspective of the leading indicators, the economic growth will further slow down. Since the beginning of this year, the growth rate of investment in fixed assets has decreased compared with the previous year, and investment growth has been rationally stabilized. From January to July this year, the area of ​​new housing starts was 922 million square meters, up 67.7% year-on-year, and down 3.7 percentage points from May. Although the manufacturing purchasing managers’ index has continuously declined since the second quarter, it remained at over 50%, reaching the highest value of 55.7% in April, falling back to 53.9% in May, falling back to 52.1% in June, and continuing to fall back to July. 51.2%. The second is the implementation of the real estate market regulation and combination policy, which will have an impact on the demand for industrial products such as building materials, household appliances, furniture, steel, and cement. Third, the expected appreciation of the renminbi and the sovereign debt crisis in Europe have increased the uncertainty in the second half of the year. In addition, the promotion of a series of measures such as the liquidation of local government financing platforms and the suppression of excess production capacity will also have an impact on the industrial growth rate in the second half of the year.

In terms of sub-industries, the raw material industry, as a key industry in the current macroeconomic regulation and control, has arduous tasks in terms of energy saving and emission reduction and elimination of outdated production capacity. At the same time, it has been affected by the weakening of investment in fixed assets and the significant increase in the growth rate in the second half of the year, especially in the fourth quarter, and the high base. The growth rate in the second half of the year will drop significantly. From January to July, the added value of raw material industry increased by 15% year-on-year, and the growth rate was already lower than the growth rate of industrial added value above designated size by 2 percentage points. The monthly growth rate showed a significant drop, and the annual growth rate is expected to be no higher than 12% of last year. Level, the average growth rate in the second half of the year is about 8%.

The equipment manufacturing industry will continue to maintain stable and rapid growth under the drive of fixed-asset investment, auto consumption and exports. From January to July, in the urban fixed asset investment, the cost of purchasing equipment and equipment continued to maintain a 20.5% growth rate on a high base last year; the automobile output reached 10.21 million units, an increase of 43.6% over the same period of last year. About 16 million vehicles, an increase of about 15% over the previous year; the industry's export delivery value increased by 29.4% year-on-year, an increase of 6.8% over the same period in 2008, reversing the continuous decline last year. From the perspective of the overall operation of the industry, from January to July, the value-added of equipment manufacturing industry increased by 22.7% year-on-year, 5.7% faster than that of all industries above designated size, and the monthly growth rate was basically in a relatively mild state. It is expected that the annual growth rate will reach 18.5. About % (13.8% last year), the second half will fall back to the 14%-15% range.

The consumer goods industry will continue to benefit from the steady growth of domestic consumption and the rapid recovery of foreign trade and exports, and maintain a stable operation. From the perspective of changes in the domestic consumer market, from January to July, the total retail sales of consumer goods increased by 18.2% year-on-year, an acceleration of 3.2 percentage points year-on-year. After deducting the price factor, the actual increase was basically the same as that of the same period of last year; household appliances to the countryside, trade-in, etc. encouraged consumption. The effect of the policy continued to show that the sales of home appliances to the countryside were 39.27 million units, and the sales amount reached 83.8 billion yuan, which was an increase of 1.8 times and 2.4 times year-on-year respectively, and the output of major home appliances products rose rapidly. In terms of foreign trade, from January to July, the export delivery value of the consumer goods industry increased by 22.2% year-on-year, an increase of 10.8% over the same period of 2008. From the perspective of the overall operation of the industry, from January to July, the added value of consumer goods industry increased by 15% year-on-year, and it is expected to grow by about 13% (10.8% last year) and about 12% in the second half of the year.

The electronic manufacturing industry has a high degree of external dependence. The export delivery value of the whole industry accounts for more than 60% of the total sales value of the industry. With the effects of the international market recovery and the expansion of domestic demand policies appearing, domestic sales, exports, and investment continue to increase at the same pace, and the industry operation has seen a clear upward trend. From the perspective of export, from January to July, the export delivery value of electronic manufacturing industry increased by 29.3% year-on-year, an increase of 15.3% compared with the same period of 2008, and was the fastest rebounding industry in the industry. From the domestic market, the number of newly-started projects for integrated circuits, flat panel displays, and new lighting materials has increased significantly. The home appliances to the countryside, the third-generation mobile communications technology (3G) commercial and new technology product markets have spurred significant growth. From the perspective of overall industry operations, from January to July, the value-added of electronic manufacturing industry increased by 19.3% year-on-year. According to the current operating situation, the growth rate of annual added value is expected to reach 15% or more (by 5.8% in the whole year of last year). About 10% increase.

Fourth, strive to adjust the structure and change the mode of development to achieve sustainable industrial development

Accelerating the transformation of development methods and advancing structural adjustment are major strategic tasks for the current and future period. At present, the industrial economic operation is in a critical period. While maintaining the steady and rapid growth of the national economy, we must pay more attention to promoting structural adjustment and pay more attention to promoting the transformation of development methods, and strive to achieve mutual promotion of economic growth and structural adjustment. In the second half of the year, we should focus on the following aspects:

(1) Maintaining the continuity and stability of macroeconomic policies and striving to achieve a shift from a rebound to a stable growth in the operation of the industrial economy

First, continue to implement the adjustment and revitalization plan for key industries, continue to implement and improve the policy of expanding consumption, and promote the consumption of home appliances, automobiles, and energy-saving products. The second is to implement the relevant provisions of the “Several Opinions of the State Council on Further Promoting the Development of SMEs†to promote the steady and sound development of SMEs and enhance the vitality of sustained economic development. The third is to strengthen the systematic, overall and relevant analysis of policies, select the right time for the introduction of policies such as price reforms of resource products, environmental protection charges, real estate tax collection, and reserve requirement ratio adjustments, and handle all aspects of conflict of interest and prevention. Due to the policy superposition effect, the negative impact on the company's business has been enlarged. Fourth, strengthen economic monitoring, forecast and early warning, closely track developments and changes in the situation, strengthen the follow-up analysis of the European sovereign debt crisis, exchange rate fluctuations, real estate market, automobile market, and external demand changes, timely discover new situations and new problems, and study and propose countermeasures and suggestions .

(II) Based on expanding domestic demand and enhancing consumer spending on industrial economic growth

The first is to continue to implement consumer policies that promote household appliances, automobiles, and energy-saving products, and actively encourage the development of new consumer hotspots and consumption patterns. Continue to adopt fiscal subsidies and tax reductions and other measures to stimulate consumer demand for energy conservation, environmental protection, and green products, and guide consumption upgrades. The second is to encourage and support enterprises to adapt to the needs of urban and rural consumption upgrades, and to produce industrial products that are marketable and can guide consumption. We will firmly seize market opportunities such as 3G development, broadband construction, and triple play, and accelerate the development of production service industries such as software services, modern logistics, e-commerce, industrial design, and industrial finance, and actively explore new types of consumer sectors. The third is to increase investment in technological transformation and optimize investment structure. As the overall scale of China’s manufacturing industry continues to expand, the supply of most products exceeds demand, and the level of industrial technology is generally low, strengthening technological transformation of enterprises is an important measure to speed up industrial transformation and upgrading and changes in development methods. It is necessary to establish a long-term mechanism for technological transformation and increase input from the central government, local governments, and enterprises to technological transformation. We will continue to increase investment in weak areas such as people's livelihood, technological innovation, and environmental protection. The fourth is to formulate and improve relevant measures to promote consumption and increase residents' income. Raise the proportion of residents' income in the distribution of national income and the proportion of labor compensation in primary distribution. Through taxation, transfer payments and other means to adjust the income distribution structure between different strata, regions, and urban and rural areas, and gradually increase the income level of low-income and middle-income residents, and fundamentally improve the residents' spending power. At the same time, continue to improve the social security system and the development of social and public utilities, and increase the residents' propensity to consume marginally.

(III) Accelerate the elimination of backward production capacity to ensure that this year's target task is completed

According to the requirements of the Central Government, we must implement structural adjustment and eliminate backward production capacity from the perspective of sustainable development strategies and national interests. Combined with the actual development of the region, we will use laws, economics, technology, and necessary administrative measures to ensure the completion of the task of eliminating backward production capacity this year. The first is to give full play to the binding effect of laws and regulations and the threshold of technical standards, and resolutely eliminate backward production capacity that does not meet the requirements. Strictly control the "two highs" and new projects with excess capacity. The second is to increase the interest compensation mechanism for eliminating backward production capacity enterprises, and promote the elimination of employees from backward production capacity through multiple channels and various means to reemploy and actively support the transformation and upgrading of enterprises. The third is to increase the administrative penalties for those regions and companies that have not completed the task of eliminating backward production capacity, and strengthen supervision and inspection to ensure that 20,087 enterprises have announced the elimination of outdated production capacity and shut down before the end of September.

(D) vigorously promote industrial energy-saving emission reduction and promote the development of recycling economy

At present, China is at an accelerated stage of industrialization and urbanization, and the demand for energy will continue to rise. China’s economic development will be subject to the dual constraints of resources and the environment, and the contradiction between economic development and energy shortages and environmental protection. More and more sharp. To this end, China can only take a new road to industrialization, develop energy-saving and emission-reduction technologies, develop a recycling economy, and improve energy efficiency, so as to relieve resources and environmental pressure and promote sustainable economic and social development. The first is to strengthen industry classification guidance, support and encourage enterprises to increase technological transformation efforts, and continue to eliminate technologically backward, environmental pollution, low resource utilization processes, technologies and equipment, and introduce advanced equipment for energy conservation and emission reduction. The second is to increase capital investment, through investment, subsidies, prices and other economic levers, from the R & D, application, promotion and other links to strengthen the guidance of financial funds to attract social capital investment, and fully mobilize the role of the market allocation of resources. The third is to establish and improve a scientific emission reduction index system, monitoring system, and assessment system to ensure that energy conservation and emission reduction achieve practical results.

(V) Actively promote mergers and acquisitions to enhance the international competitiveness of enterprises

First, we must eliminate the institutional obstacles to corporate mergers and reorganization. Clearance and abolition of various regulations that are not conducive to corporate mergers and reorganizations and impede fair competition. In particular, efforts should be made to eliminate barriers to mergers and reorganizations across regional and cross-ownership enterprises. Second, we must strengthen policy support and guidance for mergers and acquisitions. Strengthen coordination with departments of finance, taxation, land and resources, and social security, speed up the formulation of preferential policies that facilitate the promotion of mergers and acquisitions, and guide enterprises to properly resolve outstanding issues such as taxation, debt processing, and employee placement, and reduce the cost of mergers and reorganizations. To burden and accelerate the process of corporate mergers and reorganization, and continue to strengthen the guidance of mergers and reorganizations in 10 key industries such as steel and automobiles. The third is to encourage and guide enterprises to innovate systems and change mechanisms. Further improve the corporate governance structure, integrate internal industrial resources and production factors, and establish a sound and effective production and management model.

(6) To cultivate strategic emerging industries and form new economic growth points

First, we must pay attention to the integration with traditional industries. Combining the development of strategic emerging industries with the upgrading of traditional industries, increasing the use of high technology and advanced and applicable technologies to transform and upgrade traditional industries, nurturing and developing new industries in the transformation and upgrading of traditional industries. Actively promote the development of energy conservation and environmental protection, new energy, new materials, biomedicine, information networks, high-end manufacturing industries and new energy vehicles. Second, we must adhere to independent innovation. It is necessary to speed up the implementation of major national science and technology projects in areas such as new energy and new materials, overcome a number of key and key technologies that are of a global and leading role, and successfully develop a number of major strategic products with independent intellectual property rights and market competitiveness. Third, we must attach great importance to fostering the market. A good market environment and supporting measures are important foundations for the healthy development of strategic emerging industries. The huge market potential for domestic demand is also an important advantage for the development of strategic emerging industries. In the process of the development of strategic emerging industries, we must take advantage of the market, carefully study the market, and strengthen the cultivation of the domestic market. Fourth, it is necessary to strengthen the overall planning for investment in strategic emerging industries to prevent the emergence of blind investment which will lead to the emergence of new overcapacity.

years

Current sales growth rate

Â

In which domestic sales growth rate

The proportion of total sales value%

Â

Export delivery value growth

The proportion of total sales value%

2007

27.4

28.7

81.6

21.9

18.4

2008

29.3

32.2

83.4

16.3

16.6

2009

1.8

5.2

86.3

-15.6

13.7

2010

32.4

33.1

86.8

28.2

13.2

Catalytic Incinerator,Waste Gas Incinerator,Waste Pyrolysis Incinerator

Multi-Arc Ion Vacuum Coating Machine Co., Ltd. , http://www.nscoatingline.com